September Starts with a Bang

Massive sell off after a bullish close to august but internals remain bullish.

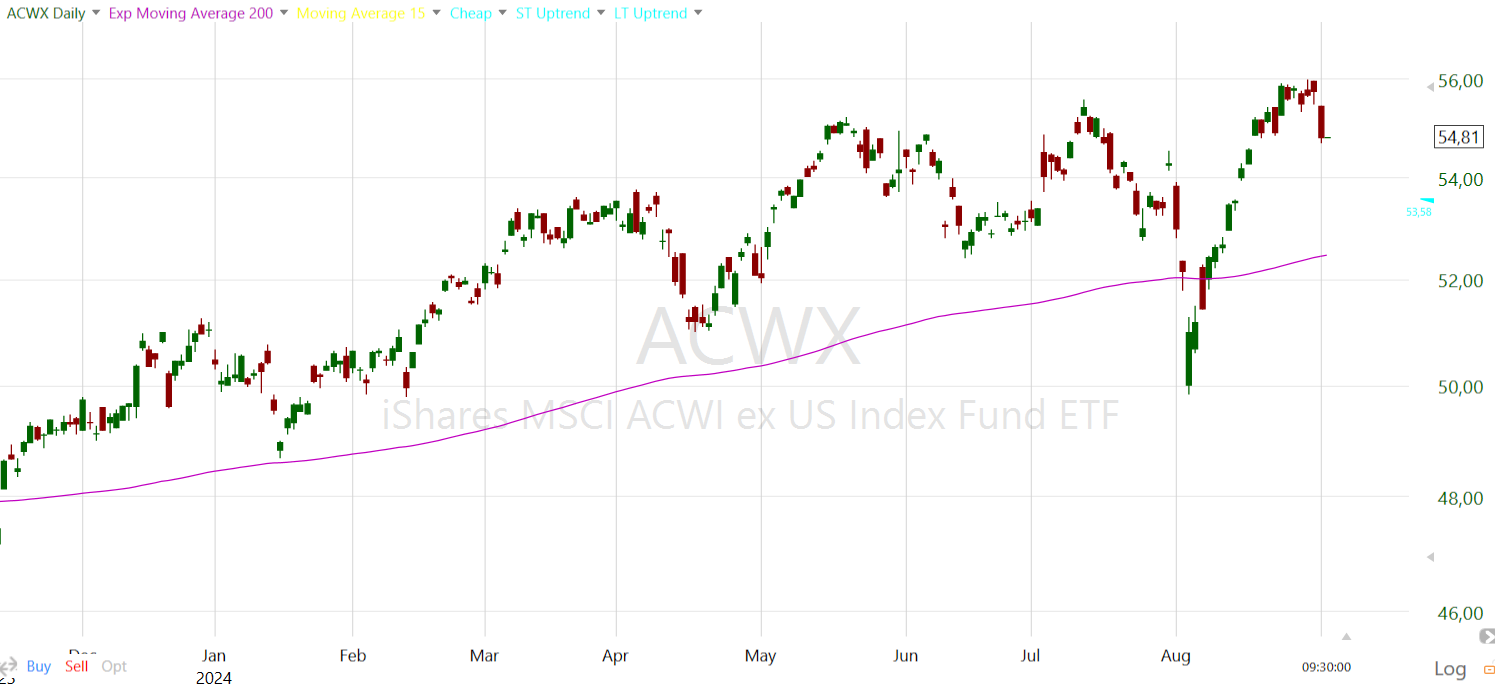

Summer 2024 has been a particularly turbulent time for the stock market, marked by significant fluctuations over the past two months. As September begins, this volatility shows no signs of slowing down. On the first Tuesday after Labor Day, the market experienced a widespread sell-off of substantial magnitude, with nearly every sector and country—aside from consumer staples—taking a significant hit.

To gain insights into what might come next, let's delve into the technicals and explore the indicators that could guide future market movements.

Long Term Trends:

The world's most significant indices are all signaling a long-term technical uptrend, a pattern mirrored by the majority of market sectors and countries globally. The classic adage, "The Trend is Your Friend," holds true when analyzing the broader market over an extended timeframe. If the market experiences a dip or correction in September, the technical indicators suggest this could present another prime buying opportunity.

Breadth Studies:

At the time of writing, breadth studies across all time frames continue to show positive signals. While short-term studies are approaching levels that could turn negative, longer-term breadth measures have remained resilient, even during the brief market crash in early August. This suggests underlying strength in the market, particularly over the longer term.

If the market were transitioning into a deep correction or a potential bear market, we would expect to see longer-term breadth studies move into negative territory. The fact that these longer-term measures remain positive indicates that, for now, the market's underlying strength is intact.

Volatility:

Volatility stands out as a concerning factor in the current market, with short-term volatility on the rise and trading above its 200-day moving average—typically not favorable signs. However, these negative signals are tempered by the fact that most major indices remain in a long-term uptrend, supported by positive breadth. This combination suggests that while caution is warranted, the overall market outlook remains constructive.

Economy:

Despite recent doom-and-gloom headlines, the U.S. economy remains robust and continues to grow. Companies are consistently beating earnings expectations, prompting analysts to revise their estimates for upcoming quarters upward. This strength bodes well for both the stock market and the employment rate.

When you factor in the likelihood of imminent rate cuts by the Federal Reserve, it becomes difficult to adopt a long-term bearish outlook on stock prices. The combination of a strong economy, positive earnings momentum, and potential monetary easing creates a supportive environment for continued market gains.

The respected economist Ed Yardeni recently shared this chart. Yardeni states the following: “Profitable companies tend to hire workers. Pre-tax corporate profits hit a new all-time high in Q2. Corporate cash flow was $3.5 trillion (saar) during Q2, matching its recent Q4-2023 record high (chart).”

Weak manufacturing numbers have been grabbing headlines, leading some to suggest that a recession is imminent. The Conference Board's Leading Economic Index has been signaling recession territory since May 2022. However, despite these warning signs, a recession has yet to materialize. On this subject, Yardeni offers the following insight: “We've observed that real GDP has been growing despite the weak readings in the M-PMI since the end of 2022. So far, both the M-PMI and Index of Leading Economic Indicators have been very misleading economic indicators indeed. They haven’t been a good recession indicator at all so far. More specifically, this indicator has been signaling a growth recession in manufacturing, yet real GDP of goods and of real consumer goods have been rising and both are in record high territory currently (chart)!”

Conclusion:

The market is currently navigating several headwinds, including elevated volatility, concerns about U.S. economic growth, uncertainty surrounding the upcoming U.S. election, and a seasonally weak period for stocks. These factors are likely to create a bumpy and potentially unsettling ride in the near term.

However, the broader outlook—both in terms of technical indicators and the overall economy—remains positive. Given this, I place high confidence in the uptrend resuming in 2024. As a result, buying the dips continues to be a viable strategy, and seeking opportunities to go long still appears to be the best approach.

That is all for today.

Best regards,

Victor Riesco, CMT